If we build it, will debt come?

According to Partech’s 2021 Africa report, Africa is officially the fastest-growing ecosystem in the world. Funding for African startups hit an all-time high in 2021, with $5.2B in equity deployed, a 264% increase year over year. The continent also saw major global investors commit considerably - through human capital (making Africa-specific hires) and investments made (welcome to the continent, silicon valley!)

Fintech is still very comfortably queen of the ball. While it accounted for only 32% of funded deals, it made up the majority of funding to the continent.

But with the rise of fintech, comes an increased need for financing - specifically debt financing. Any emerging markets investor or entrepreneur will tell you that raising debt is difficult, but it feels particularly difficult in Africa. How much debt capital does our market actually need? What’s holding us back? And if we build the rest of the ecosystem, will debt come?

Great questions - they’re the same ones we posed to two people who are pretty knowledgeable in the space. Our friends at Goldfinch, Sam Eyob, and Obinna Okwodu. Sam spent most of his career working in credit at various financial institutions such as Goldman Sachs in the UK, and Lendable, a credit fund focused on early-stage fintechs. While Obinna previously founded Fibre, a Lagos-based venture that was focused on disrupting the rental market in Africa, and worked in Investment Banking at Morgan Stanley.

Hi everyone,

Sam & Obinna here! Let’s dive in 🏊🏾♂️🏊🏾♀️:

Don’t take it from us, have a listen to the latest The Africa Playbook podcast on raising debt capital on the continent. You can get a diverse range of opinions from fintech operators, advisors, and equity investors.

Special thanks to Sam Eyob, Umulinga Karangwa and Jesse Ghansah for sharing their knowledge and participating in this episode.

Find the episode here 👇🏾

In this piece, we’ll 🏃🏽♀️🏃🏾♂️ 💨 touch on:

👩🏽🏫How much debt has been raised, and what's the gap?

💸 Is debt for everyone, and what are the challenges to raising it?

👀 Where can the debt come from?

👩🏽🏫 How much debt has been raised?

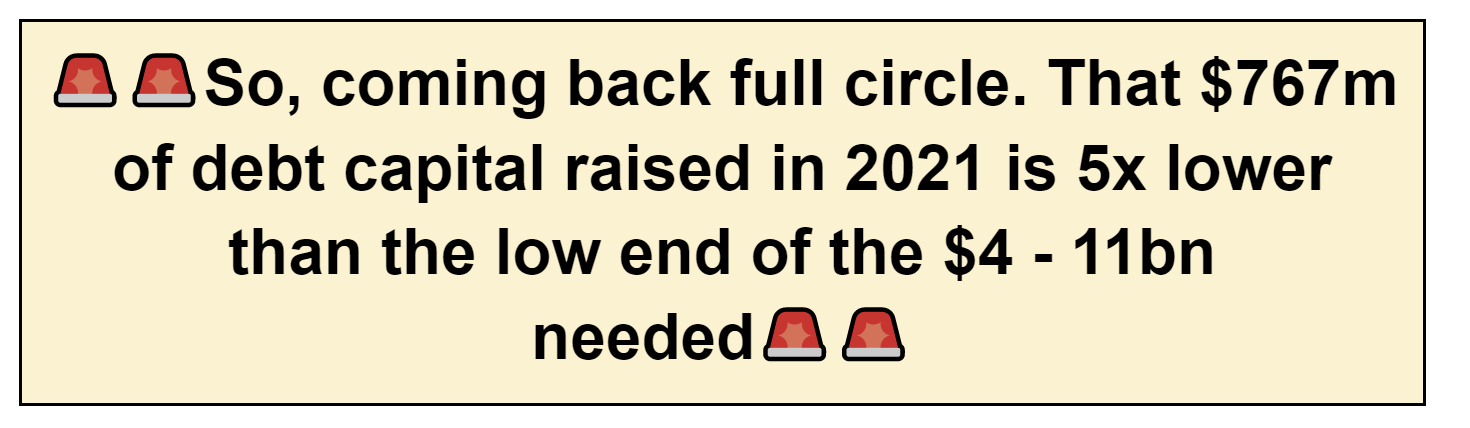

According to the Partech 2021 Africa report, $767m was raised over the course of 2021, that’s ~13% of the total capital (Equity + Debt) raised in 2021. That then begs the question, is 13%, a lot, a little, or just right?

Founders, here’s an insanely oversimplified framework for assessing how much debt you’ll need:

Is your business capital intensive?

In plain terms, does the product and/or service you provide require you to put up capital to accomplish whatever you’re building? To illustrate our point, let’s look at 2 examples (Company A and Company B) that have different capital needs:

Company A is a Software as a Service (SaaS) platform that sells lead tracking software to sales teams at mid-sized firms. They collect a standard fee on a monthly basis for their software. This business does not require any debt financing to carry out its primary operations. The founders could raise debt instead of equity but they don’t need it to make their product work.

Company B is building banking for SMEs, and their primary product is a credit line for SMEs to purchase inventory. Company B is a capital-intensive business - it needs debt to be able to carry out its primary operations, i.e. lending to SMEs.

What’s a relatively safe amount of debt to raise?

In the finance world, there’s a term called Debt to Equity (D/E) which is one of many ways to evaluate how much leverage you are taking. As a simplified example, imagine a car loan where the car costs $100. A lender generally won’t provide you the whole $100 as they want to ensure you’re incentivized to repay the loan. Most lenders require some sort of down payment which could be thought of as equity, or “skin-in-the-game”. In our car loan example, let’s say they require you to pay $25, and they cover the other $75 (i.e. $100 = $25 from you + $75 from the lender). In this instance, you now have a 3x ($75/$25) D/E ratio.

So back to the question, what’s a safe amount? For growing businesses, especially Series A and beyond who require debt to make their product work (like Company B in our example), a D/E of 2 to 5x would be expected (the higher you go, the riskier things get).

So where does the continent sit relative to the two questions above?

Is your business capital intensive?

We’d wager that over 70% of the new ventures on the continent aren’t SaaS platforms, and similar to Company B, require some debt capital to make their product work. e.g. ventures providing loans to small businesses, last mile distribution/mobility services, payment platforms.

What’s a relatively safe amount of debt to raise?

At a 2-5x D/E, and given the ~$3bn in equity raised by fintechs over 2021, that indicates our market needs $6 - 16bn in debt capital. Even after scaling this down assuming only 70% of ventures are capital intensive (i.e. like Company B), it still implies $4 - 11bn in debt capital is needed.

So what does this mean for 2022? Taking a look at Max Cuvellier’s recent 1Q’22 funding raised (Tick... Tick... Boom! Q1 results are in), we’ve got a LONG way to go. The first quarter of 2022 saw $1.8bn raised on the continent, meaning these teams could need ~$2 - 6bn of debt capital to scale!

💸 Is debt for everyone, and what are the challenges to raising it?

Let’s start off by stepping into a debt investor’s head. With the significant increase in capital flowing into our market, equity rounds are closing faster than ever. The debt space is a VERY DIFFERENT game given the calculus debt investors are benchmarking to.

● Equity Investor: Betting on a variable return, and ideally hope to +10x their investment. They’re betting on unlimited upside.

● Debt Investor: Generally invest for a (mostly) fixed return. They’re betting on the outcomes with a limited upside.

To illustrate this - here’s a simplified analogy:

An equity investor can invest $100M across 10 companies, and even if 9/10 go to zero, with 1/10 being a 10x winner, the investor actually loses nothing and ends up with $100M.

Conversely, a debt investor can invest $100M across 10 companies at 10% interest rate. If just 1/10 goes to zero, and the other 9/10 pay perfectly, the investor ends up with $99M!

In summary:

Equity Investor: made 90% bad choices, and 10% good choices, and didn’t lose 💰

Debt Investor: made 90% good choices, and 10% bad choices, and lost 💰

It’s important to understand this point as it explains why raising debt can be such a grueling experience - with the process moving at a snail’s pace relative to an equity raise – and often requiring a heavier burden of diligence.

That said, here’s a great 🧵 from Goldfinch summarizing the various issues with the private debt markets:

👀 Where can the debt come from?

So where is all this capital going to come from? There are lots of sources, but most fall under the following (non-exhaustive) list:

Banks - Here is a list of Africa’s largest banks, by assets in Africa (YE’21). While they clearly have enough capital to help fuel growth, it’s almost become a trope that banks either A) prefer to invest in real estate, or B) government bonds which are no brainers given the double-digit yields.

Local Capital Markets - There’s a host of Pension, Life Insurance, and Community/Collective Investment Schemes (e.g. SACCO’s) that act similarly to Banks in terms of where they place their capital, ultimately investing in the “safest” assets such as government bonds and real estate.

Impact Investors - The continent has a slew of private, and non-African governmental bodies (e.g. Developmental Financial Institutions) who are deploying capital into the continent as a mix of debt, equity, grants, and infrastructure financing. That said, the latest list of debt investors focused on Africa amounts to just 25 based on Impact Assets’ rigorous standards.

✨Defi✨ - Or decentralized finance (DeFi) as it’s more commonly referred to is a new path for debt mark. Here’s a short summary of DeFi via Investopedia:

“Decentralized finance (DeFi) is an emerging financial technology based on secure distributed ledgers similar to those used by cryptocurrencies. The system removes the control banks and institutions have on money, financial products, and financial services.” Bridging this back to the continent, you can also read up/watch an explainer on DeFi from Justin Norman at the Flip here.

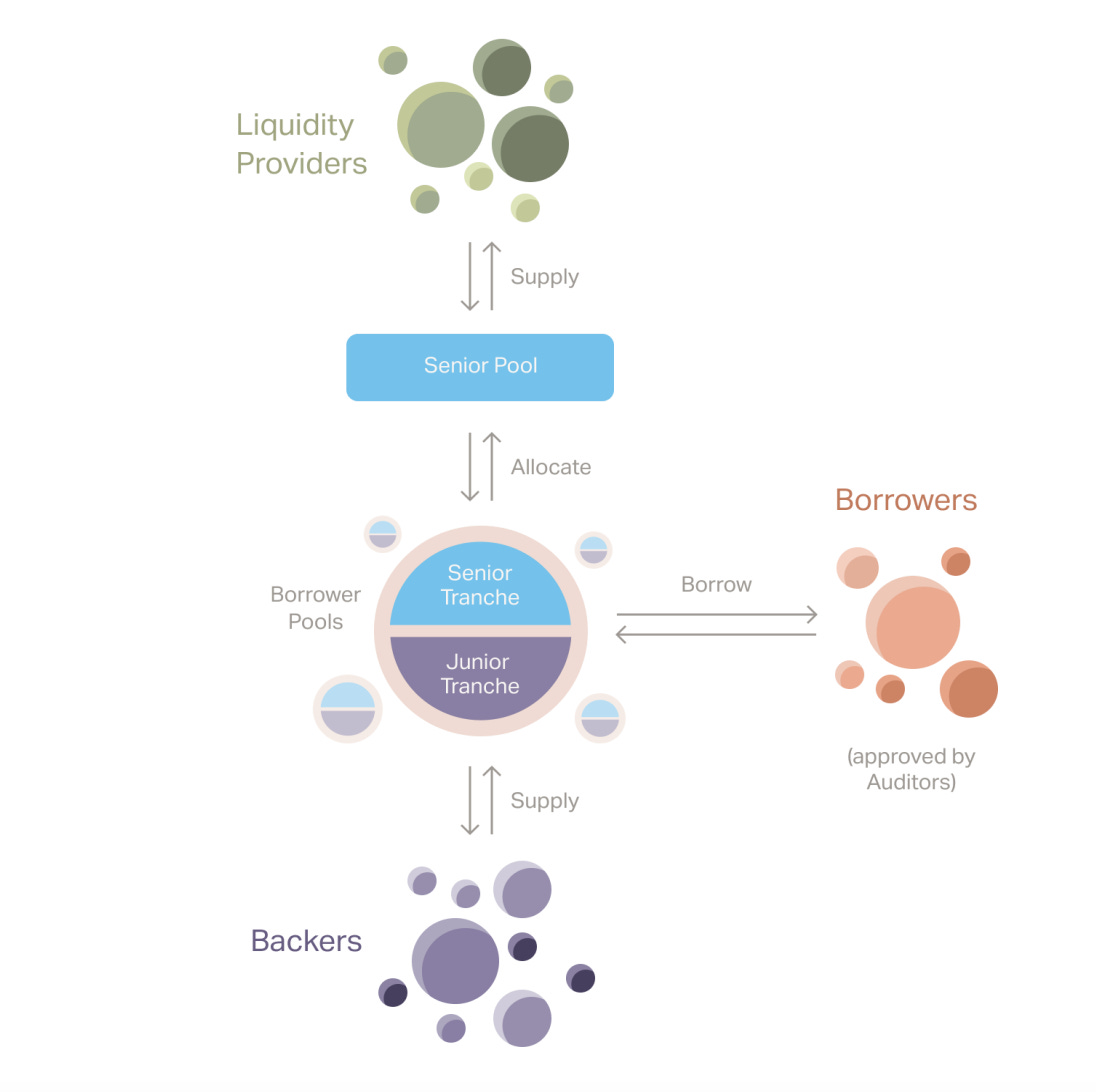

Goldfinch is an example of a decentralized credit protocol using crypto to empower financial inclusion around the world. It allows crypto lenders to earn stable, uncorrelated crypto yields by facilitating real-world loans. The protocol, whose basic mechanics are outlined below, is a global, decentralized network that allows anyone to be a lender, not just banks.

Liquidity Providers supply capital to the Senior Pool. The protocol automatically allocates the Senior Pool to the senior tranches of Borrower Pools.

Borrowers propose pools (with terms like the interest rate) for the Backers to assess

Backers supply capital to the junior tranches of Borrower Pools.

It’s important to note that crypto still faces many challenges in Africa, chief among them, an uncertain regulatory environment (as shown in the graph below).

Source: Baker Mckenzie

However, there’s no denying the potential of DeFi in a market like ours - particularly as it relates to unlocking debt capital. Goldfinch’s loan book recently hit $100M, up from $1M in February 2021. The platform has deployed loans to borrowers across five continents, covering 28 nations, including Brazil and Kenya.

🚀So where do we go from here?

Given that a majority of businesses in our market are capital intensive, our need for debt will only continue to grow. Particularly as we continue to see fintech take the lead in our ecosystem. In the words of Jesse, founder and CEO of Float:

Our ecosystem’s growth is being held back by a lack of access to debt capital. We need more debt capital and debt allocators. Traditional institutions need to take a more active role in engaging with the ecosystem and reallocating local capital to fill this outsized need for debt. At Goldfinch, we’re excited to play our part in unlocking more debt capital for the continent.

Onwards, Africa!