She's not a Country, She's a Continent

She's not a Country, She's a Continent

While the opportunity in Africa is the sum of her countries, evaluating the continent solely as a single market oversimplifies the opportunity and underestimates the risk.

Africa is often referred to and analyzed as a country or single market, when in reality, it’s a cluster of them. Its population of over 1 billion is spread across 55 countries with different infrastructure, currencies and regulations. Over the last decade, increased internet connectivity and mobile penetration has catalyzed the continent’s technological development, and nurtured a burgeoning startup ecosystem. According to the e-Conomy Africa report, the continent’s internet economy will be worth $180 Billion by 2025, and $712 Billion by 2050. While the opportunity in Africa is the sum of her countries, evaluating the continent solely as a single market oversimplifies the opportunity and underestimates the risk.

Market fragmentation is arguably the biggest challenge entrepreneurs have to navigate when building for the African market. A cluster of fifty five different countries means that most startups will need to expand beyond their home country in order to meaningfully penetrate the total addressable market. However, expanding to different countries can be costly and time consuming. Companies have to navigate new regulations, different infrastructure, currency risk, among other things. They also have to carefully weigh the optimal time for expansion, and evaluate which countries to expand to, often with very limited information.

This friction is attributable to both a nascent ecosystem and a shortage of capital. The first wave of innovators are still learning the optimal way to scale across borders, but their progress will likely be slowed by a lack of sufficient capital. Expansion for startups in the US is relatively frictionless because it’s a well capitalized singular market, with high internet connectivity and smartphone penetration. Placing the expectations of the US tech ecosystem on Africa is premature. The African ecosystem is in much earlier stages and still evolving. Building for Africa will become more frictionless over time, as more capital flows into the market, and best practices for expansion are established.

So why should you pay attention now? Why not wait until things become more frictionless and invest then? Because today’s entrepreneurs are building the infrastructure for everyone else. They will become the backbone of the ecosystem, and our first African giants are undoubtedly among them.

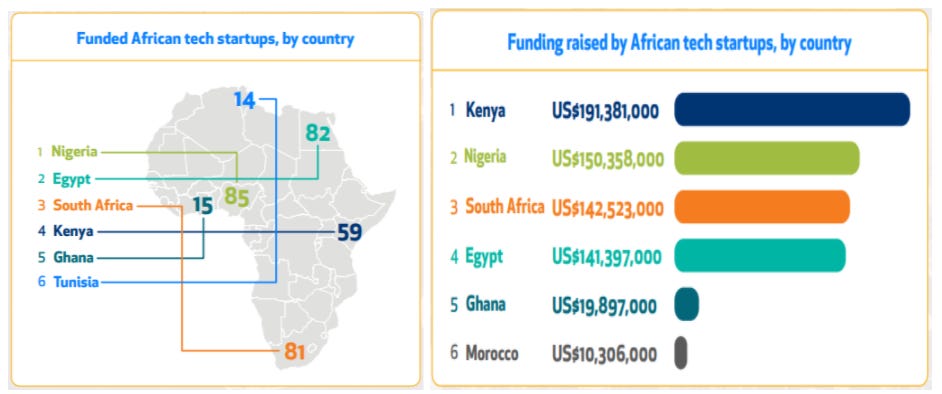

It is important to note that technological development and growth have not been proportional across the continent. There are only a handful of countries that claim the majority of funding, and have emerged as key tech hubs.

What’s in a hub?

There are two primary parameters that are shaping Africa’s tech hubs: capital and the developer population.

Capital inflows validate the ecosystem and encourage more entrepreneurship. In light of the expansion risk, there is a bias towards funding startups with large home markets. We call this The Major Market argument. Although it puts smaller markets at a significant disadvantage, there is some merit to this rationale. Companies with large home markets may not need to expand to as many other countries. As a result, most of the funding on the continent goes to larger markets like Nigeria, Egypt, South Africa and Kenya.

It is worth noting that there is a tendency to conflate population with market size. While this population based market sizing framework works fine in more developed markets, it falls apart in emerging markets. All else equal, a country with 100 million people and 20% smartphone penetration won’t yield as large a potential user base for a mobile app, as a country with 50 million people and 100% smartphone penetration.

Source: Disrupt Africa 2020 Report

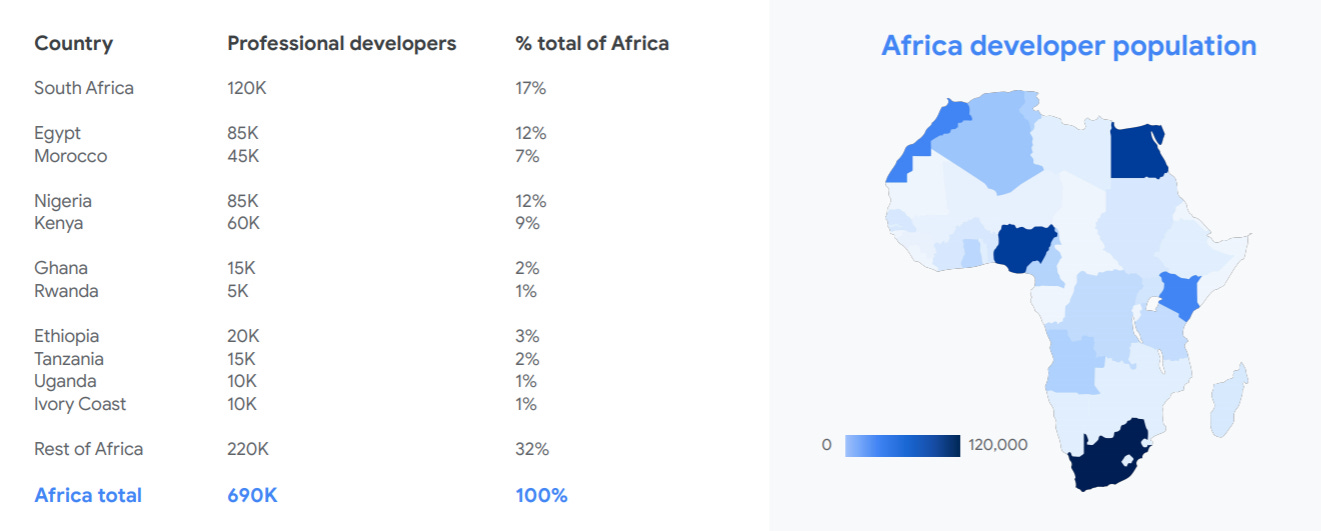

Developer population is another key factor that has played a role in defining Africa’s primary tech hubs. This is intuitive as developers are the backbone of any tech ecosystem. There are approximately 24 million developers globally, and according to the e-Conomy Africa report, Africa is home to 690K of them. The growth of the developer population will continue to play a critical role in creating and shaping tech hubs.

Source: Google/IFC e-Conomy report

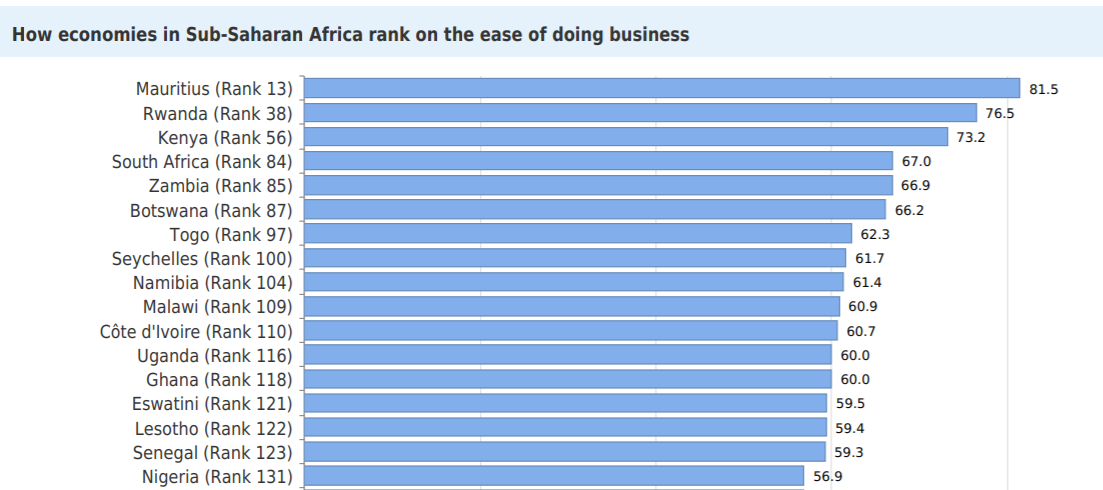

A tertiary parameter that we considered but didn’t formally include is the ease of doing business. We expect this will play a more significant role over time as the ecosystem matures and there is less emphasis on larger markets or expansion risk. However, it is worth noting that both Kenya and South Africa are ranked relatively high in the ease of doing business index.

Source: World Bank Doing Business Report 2020

To categorize the stage of development of the emerging tech hubs in Africa, we used a framework popularized by real estate investors to evaluate how developed a city is, the Tier System (Tier 1, 2, 3).

Please note: This is by no means an exhaustive analysis or list. We expect to refine our framework and update this regularly. We’re excited to hear your input as well - so please share your opinions with us on twitter @Africa_Playbook.

What We’re Reading About:

The Chicken or the Exit: Great analysis on the misplaced pressure to produce exits in the African tech ecosystem.

African Continental Free Trade Area (AfCFTA) agreement: Paying close attention to how this will impact trade in Africa over the short term and long term.

Onwards, Africa!